The Legislative decree No.142 dated November 29th 2018 adopted EU ATAD directive (acronym of “Anti Tax Avoidance Directive”), by modifying definition parameters of industrial and commercial holdings.

This modification occurred by introducing article 162-bis in the Income Tax Code (TUIR), whose result was a widening of industrial and commercial holding groups. The previous definition of industrial and commercial holding also included those subjects that, according to accounting data of the last two financial years, have the following characteristics:

- total amount of financial assets higher than 50% compared to total assets;

- total amount of revenues deriving from financial assets higher than 50% compared to total earnings.

WHICH KIND OF COMPANIES ARE INCLUDED IN THE NEW DEFINITION OF INDUSTRIAL AND COMMERCIAL HOLDING?

The new definition of industrial and commercial holding will attract a higher number of companies:

- the composition of the profit and loss account is no more so important;

- the “surveillance period” only refers to one fiscal year;

- companies that do not own shares but perform financial activities for the group are included (so called “assimilated subjects”).

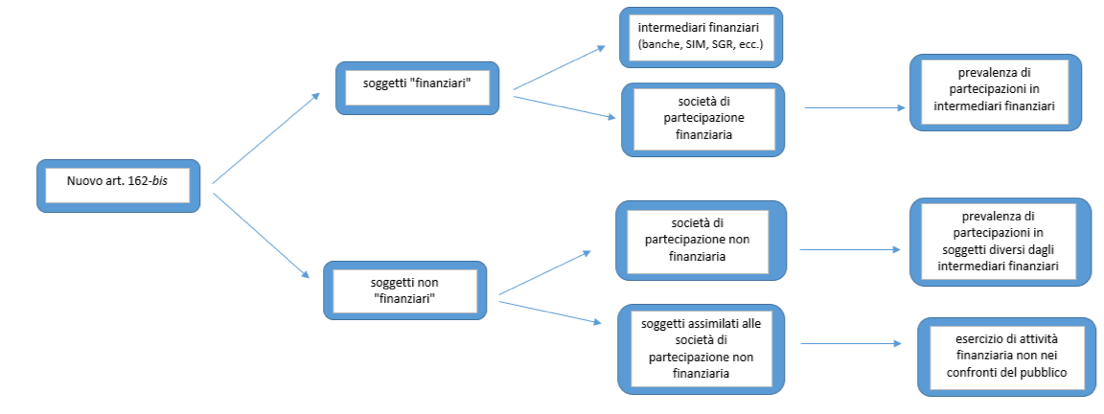

The new article 162-bis can be already applied to balance sheets that were closed within December 31st 2018 and defines financial intermediaries and the holding company as follows:

- Financial intermediaries: subjects that mainly perform their financial activity for public entities, as defined by article 106 of the TUB – Consolidated Banking Act (e. g. banks);

- Financial holding company: companies that mainly own shares of financial intermediaries, as indicated in the previous point;

- Non-financial holding company (industrial and commercial holdings) and assimilated.

Definition of non-financial holding company

- Companies that exclusively or mainly perform activities related to equity participation as regards subjects that are not financial intermediaries;

- Companies that do not perform financial activities with public entities, or, even if they do not own shares, they objectively perform financial activities (e. g. Credit agreements, Treasury) with reference to the group they belong to.

CONSEQUENCES RELATED TO THE WIDENING OF INDUSTRIAL HOLDING GROUPS

- the company will be subjected to communications by the tax register;

- registration to REI (Registro Elettronico degli Indirizzi – Electronic Register of Addresses);

- CRS and FATCA communications.

Another consequence refers to new way to calculate IRAP (regional tax on production) according to article 6 paragraph 9 of the Legislative Decree 446/97. When you calculate the production value, as established by “non-financial subjects”, you have to add the difference between:

- interest receivable and similar income;

- interest payable and similar expense.

After having calculated this result, you have to apply a higher rate compared to the ordinary rate that depend on the region. As regards the possibility to deduct interest payable, non-financial holdings apply the ordinary ROL system and, as a result, they are not excluded, like all other financial intermediaries.

BUDGET FOR NON-FINANCIAL HOLDINGS

Non-financial holdings and other similar subjects draw up their budget according to regulations established by the Civil Code, integrated by national accounting standards. Moreover, they do not adopt the same budget schemes of financial intermediaries according to Legislative Decree No. 136/2015 and to IFRS.

Companies that own shares (or those companies that – even if they do not own shares – provide financial services to other companies of the group) should check if they meet all requirements to be defined industrial and commercial holdings. If yes, they will be asked to comply with all necessary requirements with regard to the Tax Register within the end of the following month after that 2018 budget was approved (May 31st 2019 for companies with solar accounting year whose budget was approved on April 30th 2019).